Month: November 2017

15

Nov

You’re in Control with Mortgage Advice and Options

Posted by: Jennifer Koop

ADVICE AND OPTIONS MEAN YOU’RE IN CONTROL

Today, you and your spouse go looking for a new home. You’re excited because after years of scrimping and saving, you can finally afford your own place.

Today, you and your spouse go looking for a new home. You’re excited because after years of scrimping and saving, you can finally afford your own place.

You’ve engaged a realtor and he’s called you to say that he’s found your new home. You visit the property and while its not perfect, your realtor insists that this is the home for you. He says there’s nothing else available that’s better suited and urges you to make an offer. He mentions at one point that he’s actually the owner of the property he’s showed you. You make an offer at the price he suggests and, hey presto, the offer is accepted!

You move in at the end of the month, happy that you’ve at least got a roof over your head.

It all sounds pretty unbelievable, doesn’t it? You can’t really imagine doing that, can you?

Let’s look at a similar scenario; one where you make a very similar choice.

A month or two earlier, you casually mention to your mum and dad that you’re going to start looking for a home. They’re both pleased and proud – they ask about your mortgage financing – and recommend you go see their account manager at Big Blue Blank.

Like most Canadians, you prefer going to the dentist over applying for credit, so after you meet with Cal from Big Blue, you’re pleased and relieved when he calls you later that day to say you’ve been pre approved for financing at a fixed rate. He’s even guaranteed the rate for 90 days! When you end up buying that not so perfect home, the mortgage is in place in a blink of an eye.

This time, the whole scenario is way more familiar, isn’t it? Why is the second scenario any more acceptable than the first?

A Mortgage Brokers’ value proposition is based upon the ability to offer independent advice about multiple products provided by multiple lending partners.

How we demonstrate that proposition is by providing both advice and options; advice on not only obtaining the right financing, but also repayment strategies and strategies to handle a changing interested rate environment.

By combining options on rates, terms, repayment privileges and to minimize penalties, we provide you with the one thing you didn’t get in either of the two scenarios – informed choice.

Dealing with a broker, any broker, gives each of us back something we are always looking for; control.

As always, if you have any questions or need help contact a Dominion Lending Centres mortgage specialist.

Thank you to our own Jonathan Barlow, Dominion Lending Centres, Mortgage Professional for writing this article

10

Nov

4 COMMON FINANCIAL MISTAKES EVERY SMALL BUSINESS OWNER SHOULD AVOID

Posted by: Jennifer Koop

4 COMMON FINANCIAL MISTAKES EVERY SMALL BUSINESS OWNER SHOULD AVOID

Every entrepreneur and business owner will make a few financial mistakes during their journey. Those who aren’t savvy in accounting often overlook the need to brush up on their financial IQ. Truth is, these little financial errors can lead to some serious cash flow problems if you aren’t careful. Here are four financial mistakes you can easily avoid so you can protect your bottom line.

Late payments

Nobody is fond of paying bills. We tend to put them off until the last minute for short-lived peace of mind. This applies to all business owners when it comes to both your account payables and receivables.

When billing your clients, it’s common to give them an extended window of time to make payments so you can foster more sales. While your clients may appreciate the flexibility this can seriously cripple your cash flow. I generally suggest giving your clients no longer than 14 days to pay an invoice. If you’re providing quality goods and services they should have no problem paying you within this time window.

When it comes to paying your own bills, it’s important to follow the same principles above. This is especially the case if you’re operating off borrowed money. Paying an invoice late may result in a few unhappy emails, but when it comes to paying off your debts you need to always be on time. Even one missed payment can severely harm your credit score.

The best way to stay on top of these is to use an online payments solution that offers online invoicing and accounting features. This way all of your bills are organized and can be accessed anywhere at anytime.

Forgetting to have an emergency fund

Every successful entrepreneur will probably tell you that hindsight is 20/20 and foresight is … well you just never know what’s going to happen. Every business will have to pivot and there will always be unexpected hurdles. That being said, it’s absolutely imperative that you have your contingency plan, especially when it comes to finances. I recommend that every business owner has a three-month emergency fund at least.

You should start putting money away into your emergency fund as soon as the cash comes in. No matter the size of your business you should learn the art of bootstrapping and staying lean. The more money you put away, the more you’ll force yourself to get by with what you have. The majority of startups fail due to the lack of or misuse of capital. Having an emergency fund gives you a bit more runway when disaster strikes.

Failing to separate business funds from personal funds

This is one of the most common and dangerous pitfalls in small businesses. Small business owners often put their lives on the line for their business, literally. This is a big no-no. When starting a business it’s important to immediately separate your personal finances from your business finances. If you’re like any other entrepreneur it’s going to take more than one go to be successful. That being said, you definitely don’t want a failed business to tarnish your financial reputation.

Start by opening up a business bank account and apply for a business credit card to keep track of expenses. Make sure you’re only using your business credit card for business expenses and vice a versa. Failing to separate the two can also lead to complications around balancing accounts, filing taxes, measuring profits and even setting clear financial goals. Do yourself a favor and avoid mixing these expenses.

Spending too much time on non-cash-generating activities

It’s a given that you most likely won’t see an ROI on every activity you do when running a business. That being said, it’s important to distinguish which ones have the highest chance of eventually generating some cash flow. When it comes to time tracking and time management, it’s important to pay close attention to your productivity levels.

Everyone has 24 hours in a day, some decide to work smarter than others and that’s why they become successful. Know that time is your most valuable asset and treat it as such. Remember, it’s okay to say no or to turn down meetings that you know provide little to no value for your business. There’s no need to take or be present on every phone call either. Being able to identify what brings true and tangible value to your business is a key to success.

Try your best to follow the 80/20 rule. There are likely three to four activities in your business that generate the most cash. Once you identify these activities, create a habit of spending 80 percent of your time doing these tasks and save the rest of your time for other miscellaneous jobs. If you’re able to get really disciplined around this strategy, it will surely pay off.

It takes years of practice to improve your financial literacy. Although most lessons in finance are learned the hard way, it’s important to learn them nonetheless. Take note of these four common financial mistakes and do your best to avoid them. Contact Dominion Lending Centres Leasing if you have any questions.

Thank you to Jennifer Okkerse, Dominion Lending Centres – Director of Operations, Leasing Division for writing this article.

7

Nov

The New Normal – Mortgage Guidelines

Posted by: Jennifer Koop

THE NEW NORMAL

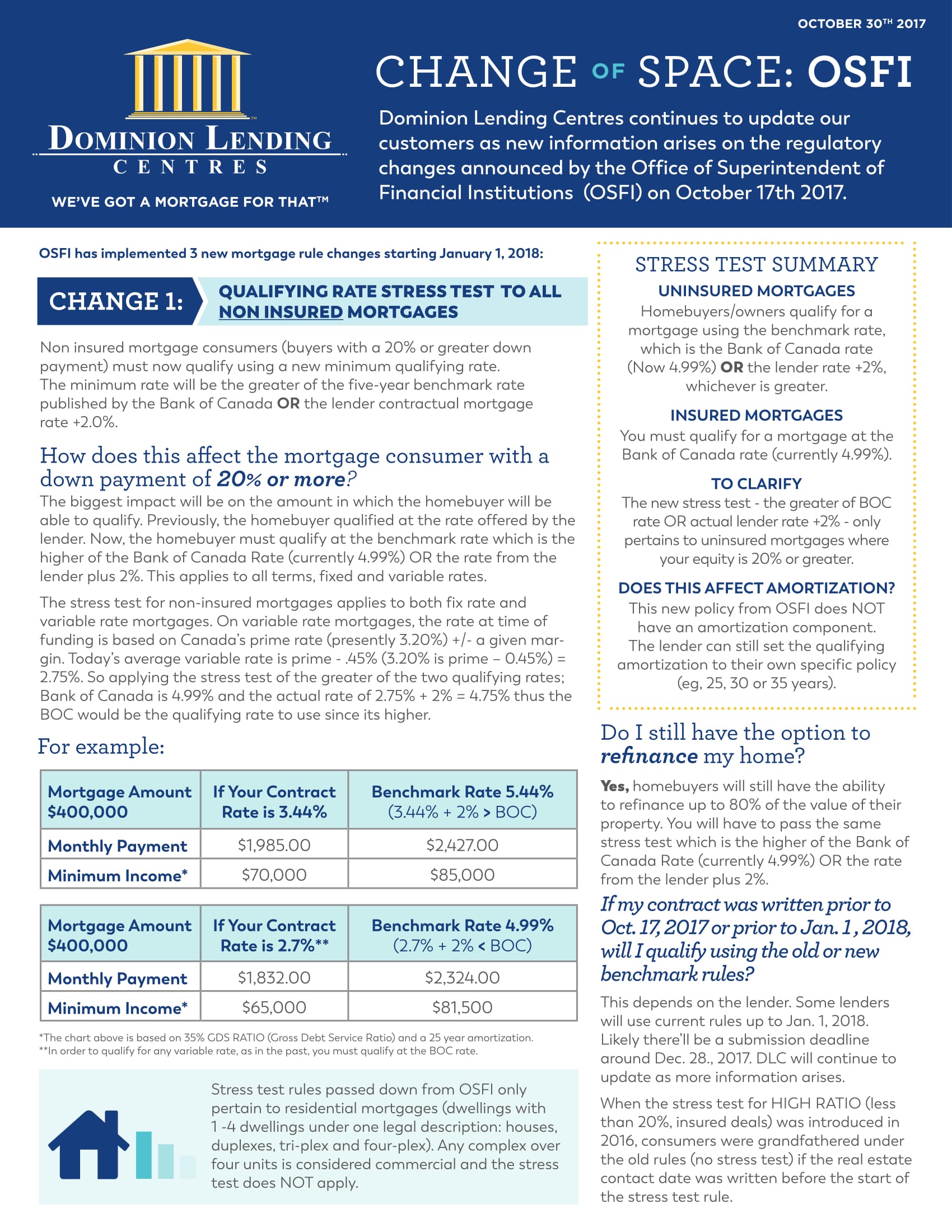

’Tis the season… this was no surprise here! The latest round of mortgage guidelines has been announced by OSFI, or Office of the Superintendent of Financial Institutions. As of January 1, 2018, all conventional or uninsured mortgages will have to qualify at the Bank of Canada 5-year fixed rate or the contractual rate + 2%, whatever is greater.

What does this mean? Nothing for anyone wanting to renew or buy real estate with less than 20% down.

But anyone wanting to access their equity might just have to consider a slightly lower amount. And those wanting to purchase real estate with 20%+ down may need to adjust their expectations or relocate their search area.

Regardless of your scenario, there will still be options to exercise.

Next question on many people’s minds is how this will affect prices. Based historical data, I predict that there will be very little decrease in prices. Most people thought the ‘bubble’ was going to explode. Most comments were, “It just has to, how can prices continue to increase?” Well guess what… prices have continued to increase. Some market segments will experience a slight softening, but nothing drastic.

Here is a list of changes issued by OSFI since 2006. Did any of them bring prices down?

2006

Maximum amortization 40 years

100% financing, 0% down payment

2008

Maximum amortization 35 years

Maximum 95% financing, minimum 5% down payment required

2011

Maximum amortization 30 years

Refinance maximum 85% of the market value

2012

Maximum amortization 25 years

Refinance maximum 80% of the market value

If mortgage insurance is required, then the maximum purchase price of the owner-occupied home is $1,000,000

2015

Minimum down payment – 5% of the first $500,000 and 10% on the portion remaining

2016

Qualification rate increases to Bank of Canada benchmark rate for all insurable files (less than 20% down)

2017

Conventional (20% down or greater) stress test increases to contract rate plus 200 basis points (2%) or the Bank of Canada benchmark rate, whatever is greater

2018

What will happen in 2018?

There is no need to slam your fist on the panic button. This is simply the new normal for mortgage finance consumers. The sun will still rise in the east and set in the west. The earth will continue to rotate in a counterclockwise direction. People will still buy and sell real estate. Those consumers with available equity will still have access to it and borrowers will still renew existing mortgages. If you are receiving or buying into “the world is ending” type information, please look away… it’s wrong and misleading.

Nothing changes.

If you are worried about things you cannot control, stop it! If you are going to put any energy into something, I would recommend building a bulletproof personal borrowing profile. More than ever it’s vitally important to have AAA credit, minimal-to-zero consumer debt and strong reliable income and savings. If you start with that, I can assure you everything will be OK!

If you have any plans to become an active mortgage consumer, start looking at your options now as some lenders will adopt the new rules before January 1, 2018. If you have any questions, feel free to contact a Dominion Lending Centres mortgage specialist.

Thank you to Michael Hallett Dominion Lending Centres – Accredited Mortgage Professional for writing this piece.